This article was originally published on Forbes.com.

With housing prices having just finished their eighth consecutive year of strong gains, you may be sitting on a good amount of equity in your home. Sitting on that equity can feel great. But is it the smart choice? Or, does it make sense to take advantage of record-low interest rates with a cash-out refinance and put that equity to work elsewhere? In this article, I want to provide a framework that should help you evaluate your personal situation.

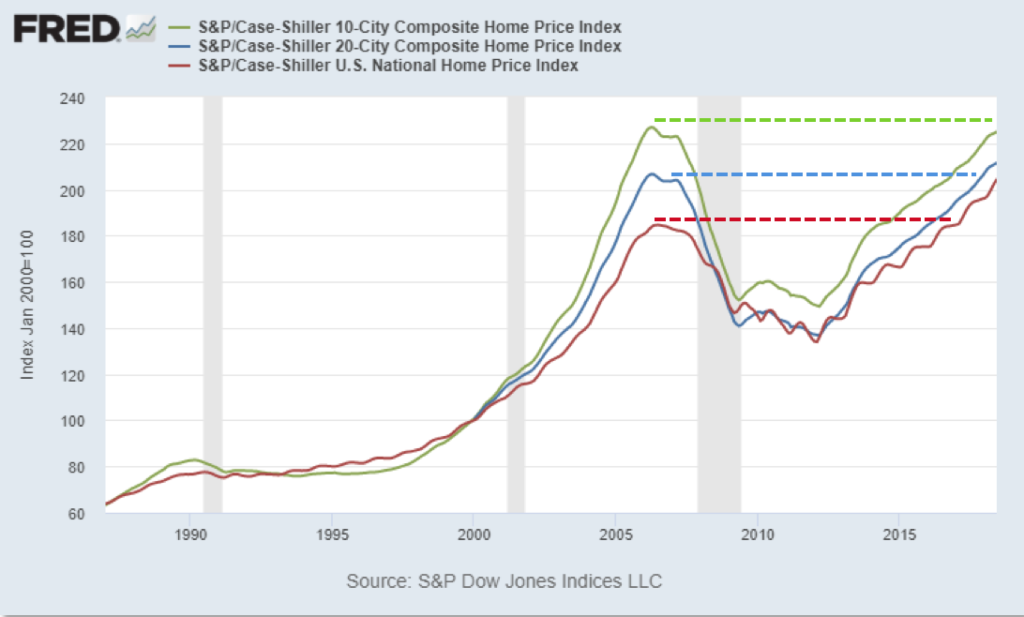

The State Of Housing Prices

Easy money policies have been in place since 2008, and their main effect has been to produce asset price inflation. Almost every asset class has been buoyed, including housing prices. Since 2013, housing prices have grown by roughly 5% or more per year, with 9.2% growth from December 2019 to December 2020.

For many homeowners, this has translated into one thing: equity. And that leads to the question: Is now the right time to pull equity out of your home?

The Case For Pulling Your Equity Out

There are, of course, a lot of things to consider when weighing the decision about refinancing or not. We’ll take a look at the risks shortly, but let’s first consider a few factors that make a case for pulling out your equity.

• Mortgage rates are at historic lows. One of the biggest factors that makes a cash-out refi so appealing is that it’s currently cheap to borrow money. With mortgage rates being this low, there are many other places you could put your withdrawn equity that could earn you much more than you’d be paying in mortgage interest.

Not to mention, because rates are so low and you can lock your rate in for a long time, a refinance at this time could mean your new mortgage payments might not increase much, if at all.

• Inflation makes fixed-rate debt attractive. Many people overlook this valuable feature of debt. If you get a 30-year, fixed-rate mortgage, your mortgage payments over the lifetime of the loan actually get cheaper in terms of real dollars. As inflation continues over those 30 years, you’re making payments with dollars that are worth a little bit less each year. Inflation is a smart debtor’s best friend. Our analysis shows inflation is not a risk right now but may be in the future. Without inflation, leveraging this debt can be a win. But if there is inflation, this could become a home run.

• Borrowed equity is tax-free, and interest is tax-deductible. Borrowing the equity in your house also provides several tax advantages. First, the equity you borrow is not taxed because it is borrowed. Second, the additional interest you pay on your mortgage is tax-deductible, making your effective borrowing cost even lower.

• Having liquidity creates opportunity. Having cash or quick access to cash allows you to take advantage of opportunity when it comes your way. This is especially true in an economy recovering from Covid-19 because there are opportunities in distressed or discounted assets on the horizon, among other things.

What About The Risks?

While the opportunities associated with pulling your equity out are strong, nothing is without risk. Here are a few scenarios where it doesn’t make sense to cash out:

• You have a high debt-to-income ratio (DTI). If you’re already overleveraged and your DTI is high, you shouldn’t do anything to increase your debt. This only exposes you to more risk.

• Your income is at risk. When leveraged folks get in trouble is when they lose the ability to service the debt. If your job or business income is at risk or unstable, this strategy is not for you.

• Your new investment vehicle isn’t stable. If you increase your debt and then invest in something volatile or unsure, you risk losing your capital and being in a worse position. Picking the right vehicle is important, so there’s a hedge of protection.

What About If We’re In A Housing Bubble?

I don’t believe the overall housing market is in a bubble or at risk of “correcting.” But I’d argue this point doesn’t matter much anyway, so long as you can still earn with the capital from your equity. Say you were to pull out money and then the value of your house tanks. Well, you might be unable to sell your home until it recovers in value, but as long as you have invested wisely, you still have that extracted capital generating additional income or growth.

This is the whole point of pulling out your equity: To put that capital to work earning for you by finding a stable, safe investment earning more than the interest rate on your loan.

Deciding Where To Invest The Money

The main factor you want to be looking for when deploying this capital is low volatility. This certainly removes things like bitcoin and other cryptocurrencies or your brother-in-law’s startup, but also the stock market and public real estate investment trusts (REITs) from the list, given the volatility.

You want to find something where the risk of loss is minimal. This could include municipal bonds, which though yields have been lower in recent years, generally see positive returns, with tax benefits too. Dividend-paying whole life insurance is also safer and can earn 5%-6%. Real estate runs the gamut of risk and return, but returns of 7%-9% are doable.

There’s Opportunity, But You Need To Weigh The Risks

The short version of this is that when done wisely, pulling out your equity can provide an opportunity to increase your net worth and cash flow, though I recommend you weigh the risks and make sure you have a safe, reliable investment vehicle to put your equity into.

If you’re interested in other ways to invest passively in real estate, read this article.

The information provided here is not investment, tax or financial advice. You should consult with a licensed professional for advice concerning your specific situation.